Are you one of the 80 percent of Americans that are in debt?

When you’re faced with a mountain of debt, it’s difficult to think about how to get out of debt fast.

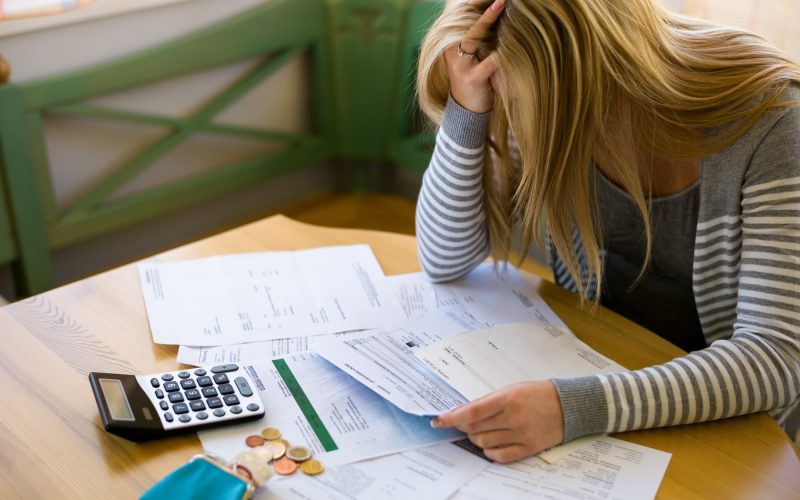

Being in debt can feel like a constant weight on your shoulders. Every financial decision you make has the specter of your debt haunting you.

To start enjoying life, you need to get out of debt fast.

But it’s not all doom and gloom! Check out our step-by-step guide on how to get out of debt fast!

Step 1 – How Much Debt Do You Have?

It’s absolutely terrifying to actually find out how much you owe. That’s why many people skip this step. But it’s important to stick with it!

Without looking at how much debt you have, it’s impossible to come up with an effective plan to pay off debt fast. You have to face up to your debts and deal with it!

If you simply bury your head in the sand, you’re playing into the game of the people you owe money. The credit card companies earn more money if you pay off a little at a time. As you continue to pay the minimum payments on a monthly basis, you falling deeper and deeper into debt.

You might be able to find out much you owe by simply calling up the credit card companies to ask. Don’t forget to also find out the Annual Percentage Rate (APR) and the minimum monthly payments.

Make sure you organize yourself with all of the details about you different debts clearly in a document either on paper or digitally.

Once you’ve found out how much you owe and faced up to your debt, the next steps are a piece of cake. Find out more about debt relief on this website.

Step 2 – Establish What is Your Priority?

Now you’re ready to get out of debt fast and set your priorities. You can’t possibly pay off all of your debts at the same time.

It can difficult to decide which debt to pay off first. This is especially the case if you’ve got lots of different types of debt from student loans to mortgage repayments to credit card bills to loan repayments.

But the answer is simple – to start with the debt with the highest interest rate.

You can save money in the long-run if you pay back more than the minimum payment each month. It sounds strange to think you’re spending more money to save more money, but it’s true.

If you have $20,000 in student loans, which has a 5% interest rate over a period 10 years of repayment. The standard repayment could be only $100 every month. But if you pay $200 in repayments every month, you’ll save much more money down the line.

Step 3 – Start Spending Less

Not all debt is bad. Getting into debt and taking out loans can be an investment in your future. For example, if you have student debt to get your law degree, or you have a mortgage to buy your first family home.

If you’re just getting into debt because you’re spending more than you can afford. You have to knock this habit quickly. It’s not always easy to start spending less when you’re used to a certain lifestyle.

You can start by canceling and throwing away your credit cards. Even though credit cards can be useful, they are often too much of a temptation to spend money you don’t have.

Even if you’re still paying off your debt and you need to keep the credit cards. You don’t have to keep the credit cards in your wallet at all times. Put your credit cards away somewhere safe.

Step 4 – Negotiate Your Interest Rate

Few people realize that it’s possible to negotiate your interest rate.

All you have to do is pick up the phone and speak to someone at the credit card company.

You have to make it clear to the credit card company that you’re serious about paying off your debt faster.

If this doesn’t work, you can say that other credit card companies have offered you lower interest rates. If the company thinks that you’re prepared to switch your balance to another credit card company, they might think twice.

Even though this tactic doesn’t have a hundred percent success rate, it’s always worth a try. You can do this with any of your debts.

If you have any success at lowering your interest rate, make sure you alter the figures on your database to match the new interest rate.

Step 5 – How to Get Out of Debt Fast

After the first 4 steps of paying off your debt fast, it’s time to actually work out how you’re going to achieve this.

You have to start by cutting back on your weekly expenses.

That might include going out only once-a-week instead of three times. Or, maybe you can start grocery shopping at the discount chain down the road rather than your regular supermarket.

Everyone has expenses that they can cut back on. It’s just a matter of deciding what you can live without.

If cutting back on your expenses isn’t enough to increase your repayments. It might be time to start thinking about increasing your income rather than reducing your outgoings.

There are many ways to increase your monthly income. You can start by asking for a pay rise at work or starting your own internet company as a side hustle.

Hacks to Pay off Your Debt Fast

With this step-by-step guide, you know how to get out of debt fast. It’s not going to be easy, but the quicker you pay off your debt, the better.

Are you struggling with your debts? Do you know of any other clever ways to save on your bills? Let us know in the comments below!